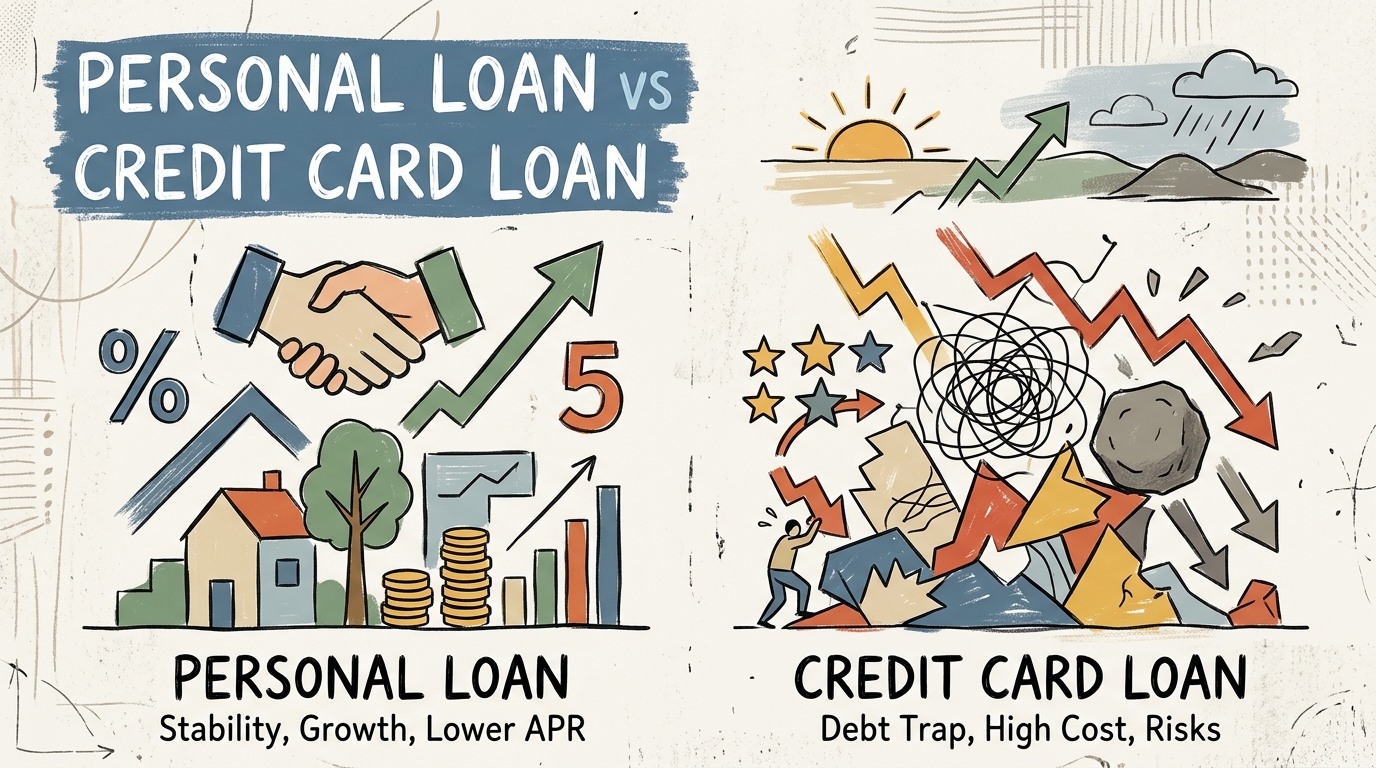

Navigating the world of debt can feel like walking through a minefield. When you face an urgent financial shortfall, the two most common options are a personal loan vs credit card loan. While both provide immediate liquidity, they operate on vastly different financial mechanics.

Understanding these differences is crucial for your long-term financial health. Choosing the wrong path can trap you in a cycle of high-interest payments that erode your savings. At money management, we believe in empowering you with the knowledge to make informed decisions.

Understanding the Debt Landscape

Most consumers view debt as a monolith, but the cost of borrowing varies significantly. A personal loan vs credit card loan comparison reveals that one is a structured financial product, while the other is a revolving credit facility. The former is designed for repayment, whereas the latter is designed for convenience.

When you take a personal loan, you agree to a fixed tenure and a fixed interest rate. Conversely, credit card debt is often treated as an open-ended line of credit. This distinction is where most borrowers find themselves in trouble.

1. Interest Rate Disparity

The most glaring difference in the personal loan vs credit card loan debate is the interest rate. Personal loans typically carry annual interest rates ranging from 10% to 18% in India. These rates are determined by your credit score and income stability.

Credit card debt, however, is notoriously expensive. If you fail to pay your full balance, the interest rates can skyrocket to 36% to 48% per annum. This is why credit card debt is often considered the most destructive form of borrowing.

2. Repayment Structure and Discipline

A personal loan enforces discipline through equated monthly installments (EMIs). You know exactly when your debt will be cleared, usually within 1 to 5 years. This predictability allows you to budget effectively.

Credit card debt lacks this structure. You are only required to pay a minimum amount, which barely covers the interest. This keeps you in debt for years, paying massive amounts in interest without reducing the principal significantly. Always check the latest guidelines from the Reserve Bank of India to understand your rights as a borrower.

3. Impact on Credit Score

Your credit score is sensitive to the type of debt you carry. A personal loan is an installment loan, which is generally viewed favorably if paid on time. It adds diversity to your credit mix, which can boost your score.

High credit card utilization, however, is a major red flag. If you consistently use more than 30% of your credit limit, your score will drop. When evaluating personal loan vs credit card loan, remember that credit card debt is a primary culprit for credit score degradation.

4. Processing Fees and Hidden Costs

Personal loans often come with a processing fee, usually 1% to 2% of the loan amount. While this is an upfront cost, it is a one-time expense. You pay it, and the rest of your tenure is predictable.

Credit cards have hidden costs like late payment fees, over-limit fees, and compound interest. These costs accumulate rapidly, making the personal loan vs credit card loan choice clear for anyone looking to minimize expenses.

5. The Psychological Trap of Convenience

Credit cards are designed to make spending feel painless. Swiping a card does not feel like spending real money, which leads to impulsive purchases. This psychological ease is what makes credit card debt so dangerous.

A personal loan requires an application process and approval. This friction acts as a natural barrier, forcing you to think twice before borrowing. When comparing personal loan vs credit card loan, the latter is clearly the more destructive option for your financial discipline.

Making the Right Financial Choice

If you are currently struggling with debt, it is time to take action. If you have high-interest credit card debt, consider taking a personal loan to pay it off. This process, known as debt consolidation, can save you thousands of rupees in interest.

By moving your debt from a 40% interest credit card to a 14% interest personal loan, you immediately reduce your financial burden. The personal loan vs credit card loan comparison proves that while neither is ideal, one is significantly more manageable.

Final Verdict on Debt Management

Choosing between debt options is never easy, but it is necessary. A personal loan vs credit card loan analysis shows that personal loans offer a structured exit strategy. Credit cards, when used as a long-term borrowing tool, are a recipe for financial disaster.

Always prioritize clearing high-interest debt first. If you find yourself needing to borrow, opt for the structured approach of a personal loan. Your future self will thank you for making the more responsible choice today.

Remember, the goal is to reach a point where you no longer need to rely on debt. Use these tools wisely, and keep monitoring your financial health regularly. The personal loan vs credit card loan debate is just one part of your broader journey toward financial independence.